Tokenized Funds: What They Are and How They Work in 2026

In his 2026 annual letter, BlackRock CEO Larry Fink compared tokenization to the internet in 1996—not yet mainstream, but about to reshape everything. His firm's tokenized money market fund, BUIDL, had just crossed $3 billion in assets under management. Franklin Templeton, WisdomTree, Apollo, and KKR had all launched tokenized fund products. BCG published research calling tokenized funds "the third revolution in asset management," projecting over $600 billion in AUM by 2030.

The tokenized fund market has grown roughly 4× since the end of 2023 and now exceeds $5 billion, with money market funds making up the lion's share. McKinsey projects mutual funds and ETFs will be the single largest category of tokenized assets by the end of the decade.

Whether you're a bank exploring digital asset services, an asset manager considering tokenized share classes, a transfer agent modernizing your infrastructure, or a fund administrator evaluating new operating models, this guide covers what tokenized funds are, how they work mechanically, the step-by-step process for launching and managing them, and what the real-world examples tell us about where this is heading.

What is a tokenized fund?

A tokenized fund is an investment fund whose shares or units are represented as digital tokens on a blockchain. The fund itself — its legal structure, investment strategy, regulatory obligations, service providers—stays the same. What changes is how investors hold their ownership stake, aligning traditional fund structures more closely with the growing ecosystem of digital assets.

In a traditional fund, ownership is a line item in a share register maintained by a transfer agent. Subscriptions, redemptions, and transfers are processed through emails, fax orders, or legacy platforms like Clearstream or FundSettle. In a tokenized fund, those same shares exist as tokens on a distributed ledger like Ethereum, Solana, Canton, or Stellar. Ownership is recorded on-chain, transfers happen electronically, and much of the administrative workflow can be automated through smart contracts. This brings better efficiency to asset management processes.

This is an important distinction: tokenization is not the creation of a new tokenized asset class. A tokenized UCITS fund is still a UCITS fund. A tokenized money market fund still invests in short-term government debt. The regulatory and fiduciary obligations don't change because the share format does.

Three ways to tokenize fund shares

The industry has settled on three main approaches:

Native tokens are the most direct method—the tokens themselves represent the fund shares. No separate paper or book-entry record exists alongside them. This is the cleanest approach and avoids maintaining two parallel systems.

Twin tokens pair traditional fund shares with corresponding digital tokens, where legal title can only transfer via the token. The token acts as a digital twin that controls the underlying share.

Indirect tokens take a different route entirely. Instead of tokenizing the fund itself, a special purpose vehicle (SPV) or feeder fund invests into the target fund, and the SPV's shares are what gets tokenized. This is common when the fund's jurisdiction or legal structure doesn't yet accommodate direct tokenization.

The choice between these depends primarily on applicable law. And it's worth noting that partial tokenization is both possible and common—a fund can add a tokenized share class alongside its existing traditional classes without restructuring anything.

How tokenized funds work

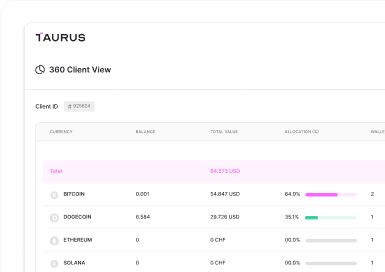

The transfer agent still sits at the center of operations. Their responsibilities—maintaining the share register, performing KYC/AML, processing subscriptions and redemptions—don't disappear. What changes is how they execute those tasks, as ownership is now represented through a tokenized share on a blockchain rather than a traditional register entry, making it more efficient to onboard investors.

Subscriptions: When an investor subscribes, the transfer agent (TA) collects their KYC documentation and, additionally, the blockchain address the investor controls. That address is scored, verified (sometimes through a proof-of-control test), and added to a whitelist embedded in the smart contract. This streamlined process helps onboard investors more efficiently while maintaining compliance. Once payment is received and the net asset value (NAV) is calculated, the TA mints the corresponding tokens and allocates them to the investor's whitelisted address.

Redemptions: The investor sends their tokens back to the TA's wallet. The TA burns those tokens and wires the cash proceeds to the identified beneficial owner. Some funds, like BlackRock's BUIDL, also maintain a smart contract-controlled pool of stablecoins (USDC) that allows 24/7 instant redemption without waiting for the next NAV calculation.

Transfers: This is where tokenization delivers its most distinctive advantage. If transfers are authorized by the fund and restricted to whitelisted addresses, they happen peer-to-peer on the blockchain. The investor signs the transaction with their private key, the ledger updates automatically, and the TA doesn't need to intervene at all. The register updates itself.

NAV and distributions: The TA continues to calculate NAV through traditional methods. That NAV can then be published on-chain via an oracle, enabling smart contracts to automate minting and burning at the correct price. Dividend or coupon payments can be distributed in cash or, where permitted, in stablecoins to the whitelisted addresses on record.

A critical design choice underpins all of this: virtually every institutional tokenized fund to date uses restricted transferability enforced via on-chain whitelisting. Only addresses that have passed KYC/AML and been approved by the TA can hold or receive tokens. This isn't a limitation—it's the mechanism that keeps tokenized funds compliant with securities law.

What types of funds are being tokenized?

Tokenization delivers the most value at the extremes of the liquidity spectrum, for different reasons.

Money market funds dominate the tokenized fund landscape today, representing over $3.6 billion in AUM. The appeal is straightforward: MMF units are low-risk, yield-bearing assets that can serve as a superior alternative to holding uninvested cash or stablecoins on-chain. As digital assets continue to gain traction, tokenized MMF units offer a more stable and yield-generating option within this ecosystem. More importantly, tokenized MMF units can be transferred between counterparties in minutes rather than days, which unlocks a significant use case as collateral for derivatives and repo transactions. MMF units are already recognized as eligible collateral in many jurisdictions—but they're rarely used for margin because traditional transfer mechanisms are too slow. Tokenization solves that.

Private equity and real estate funds sit at the other end. These are funds with high minimum investments, multi-year lock-up periods, and essentially no secondary market. If an investor in a PE fund needs liquidity, their bank, asset manager, or fund manager must manually find a matching buyer through a process that can take weeks and relies on emails and paper. Tokenization introduces the possibility of electronic secondary markets—regulated trading venues where tokenized fund shares can be matched and settled with automated delivery-versus-payment, giving investors an exit mechanism that simply doesn't exist today.

Debt and structured product funds benefit from the programmable features of smart contracts. Coupon payments, maturity events, and compliance rules can be encoded directly into the token, automating what would otherwise be manual corporate actions. Venture capital funds, hedge funds, and commodity funds are also viable candidates, each with their own specific efficiency gains from the shift to a digital format.

Benefits of tokenized funds

Liquidity and secondary markets. Tokenized fund shares are instantly transferable on a distributed ledger and can be admitted to trading on regulated digital asset venues. Each token continues to represent ownership in the fund’s underlying assets, ensuring economic exposure remains unchanged. For funds that are traditionally illiquid, this creates market access that didn't previously exist. For already-liquid funds like open-ended UCITS, tokenization offers an ETF-like trading and transferability experience without the structural requirements of the ETF wrapper.

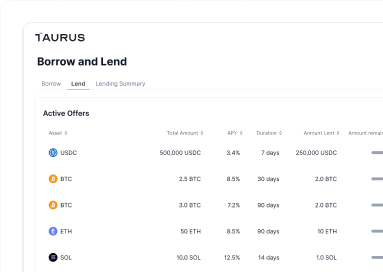

Collateral mobility. This is arguably the most significant near-term institutional use case. Tokenized MMF units settled on DLT networks can be posted, recalled, and transferred as margin far faster than through traditional processes—particularly relevant for non-centrally cleared derivatives where variation margins need to be exchanged daily or more frequently. J.P. Morgan's Tokenized Collateral Network is already live in production with buy-side firms for exactly this purpose.

Operational efficiency and cost savings. BCG estimates that fund tokenization could produce approximately 17 additional basis points in annual returns for investors by eliminating the capital drag from T+2/3 settlement periods—a gain of roughly $100 billion across the global mutual fund industry. Smart contract automation of transfer agency tasks reduces manual touchpoints, reconciliation errors, and intermediary costs. Transaction fees on secondary markets for tokenized funds can run at roughly half the cost of primary subscription/redemption fees.

Broader access. Fractionalization lets a fund manager lower minimum investment thresholds substantially. Spiko's UCITS-compliant tokenized money market funds accept subscriptions from €1,000 and have attracted over 1,100 investors—the largest investor base among tokenized MMFs on public blockchains. This model makes participating in an investment fund more accessible than ever. For developing markets where smartphone penetration outpaces bank account access, a registered digital wallet could be all that's needed to invest in regulated fund products.

The fund tokenization process

Most competing explanations of this process stay at 30,000 feet. Here's what it actually involves.

Step 1: Stakeholder alignment

The idea to tokenize typically originates with the asset manager or fund promoter. But the promoter isn't the one who executes the tokenization—that falls to the management company (ManCo) and the transfer agent. Both need to agree to proceed and be properly equipped. For regulated investment funds, the regulator must also be brought into the process. This multi-party alignment requirement is the main reason asset tokenization has historically been harder than tokenizing a simple corporate equity or SPV, and why vertically integrated players like BlackRock and Franklin Templeton moved first.

Step 2: Legal analysis and preparation

The fund's legal advisor must confirm that tokenization is permissible under the fund's articles of association and the laws of its jurisdiction. The prospectus or fund contract needs to be amended to allow shares to be issued as digital tokens, and tokenization terms or supplements must be prepared. If the investment fund is supervised by a regulator (CSSF, FCA, FINMA), the necessary approvals must be obtained. If secondary market trading is planned, legal feasibility for admission to a trading venue must be confirmed.

Step 3: Technical preparation

This involves selecting the blockchain(s), choosing and auditing a smart contract standard, and configuring parameters like the fund name, ticker symbol, ISIN, and transfer restriction rules. The ManCo or TA either handles this in-house (if they have the tools) or appoints a third-party tokenization agent. Platforms like Taurus-CAPITAL provide this capability out of the box—supporting the widest range of blockchains (EVM and non-EVM, public and permissioned), a library of audited smart contract templates including the CMTAT standard, and full lifecycle management through API or interface, with no coding required.

Step 4: Deployment

The revised legal documents enter into force, and the smart contract is deployed on the selected blockchain by the ManCo, TA, or tokenization agent. The fund is now tokenized and ready to operate.

Step 5: Ongoing lifecycle management

This is where the day-to-day work happens. At each subscription date, the TA mints new tokens and allocates them to whitelisted investor addresses. At each redemption date, tokens are burned. The TA monitors the distributed ledger, manages the whitelist as new investors are onboarded, and ensures the AML scoring of addresses remains current. For distribution events, proceeds are paid to the addresses identified in the share registry. All of this can be progressively automated through digital transfer agent smart contracts. This highlights how asset tokenization enhances efficiency across the fund lifecycle by enabling automated minting and burning based on NAV data delivered via oracles.

The process is conceptually the same regardless of fund type—EU UCITS, EU AIF, Swiss FCP, or otherwise.

Tokenization readiness checklist

Before tokenizing, confirm these six points:

- Your jurisdiction recognizes ledger-based securities (or equivalent) by law

- Tokenization provides clear benefits to the fund, its shareholders, or employees

- You have a law firm experienced in tokenization structuring

- You have a certified technology partner for issuance and lifecycle management

- You have a financial institution that can book securities for investors, if needed

- You're using standardized, audited smart contracts recognized in the market

Real examples of tokenized funds

BlackRock BUIDL—The largest tokenized fund globally at approximately $3 billion AUM. A BVI-incorporated limited company investing in U.S. Treasuries, issued as ERC-20 tokens on Ethereum with Securitize as transfer agent. Minimum initial subscription is $5 million. Transfers between whitelisted accounts are allowed at any time. A smart contract-controlled USDC pool enables 24/7 instant liquidity.

Franklin Templeton FOBXX—The first SEC-registered fund to use a public blockchain as its official share register. Over $700 million in AUM, primarily on Stellar with connectivity to Polygon, Ethereum, Solana, Arbitrum, and others. Available to individual and institutional investors through the Benji app. Peer-to-peer transfers between whitelisted wallets are permitted.

Spiko T-Bills MMFs—The first UCITS-compliant money market funds leveraging public blockchains for shareholder registers. A French SICAV structure with Twenty First Capital as ManCo and CACEIS as depositary. Open to all investors from €1,000. Shares represented as tokens on Ethereum, Polygon, Arbitrum, and Starknet. Over 1,100 investors and approximately $250 million AUM.

QoQa Equity Capital Raise—Swiss e-commerce platform QoQa tokenized participation certificates in its subsidiary QoQa Brew SA using the CMTAT standard on Ethereum. Raised CHF 1.2 million in 19 minutes from approximately 2,000 investors out of a queue of 20,000. The end-to-end process—tokenization, custody, share transfer, and investor KYC—was powered by Taurus' technology suite.

Credit Suisse, Pictet, and Vontobel Structured Products—A proof-of-concept involving three major Swiss banks issuing tokenized investment products on the Ethereum public blockchain. Settlement occurred in Swiss francs through a payment bridge connected to the Swiss Interbank Clearing system. Taurus-CAPITAL handled issuance, Taurus-PROTECT handled custody, and the instruments were traded on BX Swiss, a regulated exchange.

Regulatory landscape

Switzerland was the first Tier 1 financial center to adopt a complete DLT-compatible legal framework. Article 973d of the Swiss Code of Obligations, effective February 2021, explicitly recognizes ledger-based securities. The August 2021 market infrastructure law introduced DLT trading facilities as a new category of regulated infrastructure. Organized trading facilities like TDX allow tokenized securities to be traded while the issuing company retains its private status—no IPO required.

The European Union's DLT Pilot Regime entered force in March 2023, creating a sandbox for trading and settlement of tokenized financial instruments. Importantly, tokenized fund units are classified as financial instruments under MiFID, not as crypto-assets under MiCAR. This means they sit squarely within existing securities regulation. Caps apply: shares from issuers below €200 million market cap, bonds below €500 million issuance size, and an aggregate cap of €2.5 billion.

The United States has multiple SEC-registered tokenized funds in operation (Franklin Templeton, WisdomTree), though the broader regulatory framework continues to evolve. SEC Commissioner Peirce's July 2025 statement on tokenized securities signaled growing regulatory clarity.

Singapore has been a hub for institutional pilots through the Monetary Authority of Singapore's Project Guardian, with UBS, SBI, and Chainlink demonstrating automated fund management using digital transfer agent smart contracts.

The core principle across jurisdictions: regulation is technology-neutral. The legal obligations attached to a fund don't change because the share format does.

Who should care, and why

Fund tokenization isn't a niche blockchain field anymore. It touches every major participant in the fund value chain, and the implications differ depending on where you sit.

Banks and custodians are perhaps the most directly affected. Custody of tokenized fund shares requires new capabilities—secure private key management, smart contract interaction, multi-blockchain support—that sit outside traditional securities custody infrastructure. Banks that build or adopt these capabilities position themselves as the custodians of choice for the next generation of fund products. Those that don't risk losing mandates as asset managers move toward tokenized structures. Several of the world's largest custodians, including BNY Mellon and State Street, have already begun offering digital asset custody services for exactly this reason.

Asset managers and fund promoters stand to gain new distribution channels, broader investor access, and operational cost savings. Tokenized share classes can reach crypto-native investors, institutional treasuries looking for on-chain yield, and retail investors in markets where traditional fund distribution is limited. For managers with illiquid strategies (private equity, real estate, infrastructure), tokenization can introduce secondary market liquidity where none existed before.

Transfer agents and fund administrators face perhaps the most significant operational shift. The core TA function—maintaining the share register, processing subscriptions and redemptions, managing KYC records—doesn't disappear, but the tools and workflows change fundamentally. TAs that adopt tokenization technology can automate much of their manual processing through smart contracts, reduce reconciliation burdens, and offer real-time register visibility to all stakeholders. TAs that don't adapt risk being displaced by technology-forward competitors or by ManCos that bring the function in-house.

Management companies need to ensure their governance frameworks, prospectus language, and operational processes can accommodate tokenized shares. For regulated funds, this means engaging with local supervisory authorities and obtaining the necessary approvals—a process that has become increasingly straightforward as regulators in key jurisdictions have clarified their frameworks.

Challenges to consider

Tokenized funds are production-ready, but the ecosystem is still maturing. Interoperability between blockchains remains limited—tokenized fund units on Ethereum can't natively move to Solana, requiring burn-and-mint bridges. Secondary market liquidity depends on having enough participants; early tokenized funds may face thin order books. Operational complexity increases during the transition period when on-chain and off-chain systems must run in parallel, adding new layers to fund administration. Standardization of smart contract standards, KYC processes, and custody practices still varies across jurisdictions. And perhaps most critically, the full potential of tokenized funds depends on the availability of tokenized cash—stablecoins, tokenized deposits, or CBDCs issued by regulated institutions—to close the settlement loop entirely on-chain.

What's ahead

The next 12 to 24 months will likely see an acceleration in money market fund tokenization as more major asset managers enter the space. Collateral management and repo use cases are expected to move from pilots to production, supported by the need to maintain financial stability in increasingly digital market infrastructure.

Further out, fixed income and private credit funds will tokenize at scale, and interactions with DeFi lending and borrowing protocols will deepen.

BCG projects that tokenized funds could reach 1% of total global fund AUM by 2030—a trajectory comparable to ETFs in their first seven years after the initial 1993 launch.

The building blocks are in place: institutional-grade technology platforms for issuance and custody, clear regulatory frameworks in major financial centers, regulated trading venues for secondary markets, and major custodians entering the space.

The speed of adoption will be determined by standardization, collaboration among market participants, and the willingness of asset managers and their service providers to build network effects. Ensuring financial stability will also be critical as tokenized funds move toward becoming the default rather than the exception.

Taurus provides the integrated platform for custody, tokenization, trading, and settlements that financial institutions use to launch and manage tokenized fund offerings.

To learn more, book a meeting with our team.

Share on