Tokenization in Banking: How It Works in 2026

The world's largest banks are getting serious about tokenization in 2026.

JPMorgan's Kinexys platform processes billions in daily volume through tokenized deposits. HSBC expanded its Tokenized Deposit Service into the US in April 2026. Citi Token Services enables 24/7 interbranch transfers for corporate clients. Goldman Sachs is spinning out its GS DAP digital bond issuance platform as an industry utility. Deutsche Bank, Pictet, State Street, and CACEIS have all deployed digital asset infrastructure for custody and tokenization. BNY Mellon, SocGen, and Standard Chartered each have multiple live initiatives spanning custody, tokenized securities, and stablecoins.

A recent survey of the ten largest systemically important banks identified 24 distinct tokenization initiatives already deployed — spanning tokenized deposits, securities issuance, digital asset custody, and settlement infrastructure.

This article is a practitioner-level guide to what tokenization means in a banking context, what banks are actually tokenizing today, the operational infrastructure required, and how to build a tokenization strategy. It's written for bank executives, heads of digital assets, custody leaders, and operations teams evaluating where their institution fits in this shift.

What Tokenization Means in Banking (And What It Doesn't)

It's worth clarifying upfront: "tokenization in banking" can refer to two very different things. The first is payment card tokenization — replacing credit card numbers with substitute tokens to prevent fraud during transactions. That's a well-established data security practice.

This article is about something more fundamental. Asset tokenization in banking is the process of representing financial assets — deposits, securities, fund shares, and other instruments — as digital tokens using distributed ledger technology. The token is programmable: it carries both the asset's value and the rules governing its behavior, encoded in a smart contract.

This shift this enables is structural. Traditional banking infrastructure is account-based: transferring money involves messaging between banks to update separate internal ledgers, a process that routinely takes two or more business days (T+2 settlement) and requires manual reconciliation across siloed systems. In a token-based model, transfer and settlement can be much more closely linked, especially when the asset and payment leg are coordinated on shared infrastructure. The asset moves from one party's address to another on a shared ledger, and the transaction is final.

This doesn't mean banks are replacing their core systems with blockchains. It means they're adding a new infrastructure layer — for issuance, custody, and lifecycle management of digital assets — that sits alongside and integrates with existing core banking, risk, and compliance systems.

One critical distinction: tokenized bank assets are not automatically crypto tokens or cryptocurrencies. Tokenized deposits, bonds, or fund shares represent claims on underlying financial instruments held in custody by regulated entities. They carry the same legal protections, regulatory obligations, and counterparty relationships as their traditional equivalents.

What Banks Are Tokenizing: Five Core Areas

Banks are pursuing asset tokenization across five categories, each at different stages of maturity and each serving different strategic objectives.

A. Tokenized Deposits

Tokenized deposits are digital representations of commercial bank money on a blockchain. The deposit obligation remains with the issuing bank; the token is the on-chain format. In the financial market, these tokens act as the “cash leg” for settling on-chain transactions while enabling capabilities beyond traditional banking infrastructure, including 24/7 programmable payments, faster cross-border transfers with reduced reliance on correspondent banks, and automated smart contract-based payments.

JPMorgan was the earliest mover, with its Kinexys platform (formerly JPM Coin) now processing billions in daily cross-border volume using private distributed ledger technology. HSBC launched its Tokenized Deposit Service for corporate clients and expanded it to the US in April 2026, positioning it as a differentiator for multinational clients with complex liquidity needs. Citi Token Services allows real-time, 24/7 interbranch transfers — a function that previously took days through internal treasury processes.

The deposit token vs. stablecoin distinction matters. Both serve as on-chain cash, but from fundamentally different risk and regulatory profiles. Tokenized deposits are issued by regulated banks, may carry deposit insurance protections, earn interest, and maintain the bank-customer relationship. Stablecoins are issued by non-bank entities with reserve-backed models. As KPMG has noted, tokenized deposits are proving their worth in three areas: conditional payments, cross-border payments, and securities settlement. The two formats will likely coexist, with tokenized deposits serving regulated institutional use cases and stablecoins serving broader crypto-native markets.

B. Tokenized Securities

Representing bonds, equities, and structured products as digital tokens is one of the most mature asset tokenization use cases. The benefits are tangible: issuance timelines compress from weeks to days, lifecycle events like coupon payments and corporate actions can be automated through smart contracts, and settlement can occur atomically — meaning the exchange of the security and the payment happens simultaneously (delivery-versus-payment), eliminating counterparty risk.

SocGen's FORGE platform has issued digital bonds on public blockchains and launched the EUR CoinVertible stablecoin for on-chain settlement. Goldman Sachs built GS DAP for digital bond issuance and is planning to spin it out as an industry-wide utility. The European Investment Bank has completed multiple digital bond issuances.

In Switzerland, where the regulatory framework for ledger-based securities has been in place since 2021, banks have moved beyond proof-of-concept into live issuance. UBS (following its acquisition of Credit Suisse), Pictet, and Vontobel conducted a joint project using blockchain technology to issue tokenized structured products on the Ethereum public blockchain, with automated delivery-versus-payment settlement in Swiss francs. The issuance, custody, and asset servicing were handled through the Taurus platform (Taurus-CAPITAL for issuance, Taurus-PROTECT for custody), and the instruments were traded on BX Swiss, a regulated exchange. Separately, SCCF, a Swiss trade finance specialist, used Taurus-CAPITAL to issue a tokenized debt note on Ethereum, which was then traded on Taurus-PRIME, Taurus' regulated organized trading facility. The proceeds financed a loan to a commodity trading firm active in biofuels — a concrete example of tokenization serving the real economy.

C. Tokenized Funds

Fund tokenization — issuing fund shares or units as digital tokens — is the fastest-growing segment of the tokenized asset market. The total market has grown roughly 4× since the end of 2023 and now exceeds $5 billion, with money market funds making up the majority. BlackRock's BUIDL fund has surpassed $3 billion in AUM. Franklin Templeton's FOBXX was the first SEC-registered fund to use a public blockchain as its official share register. Goldman Sachs and BNY Mellon announced a partnership to use blockchain for tokenized money market fund record-keeping.

Banks care about this for multiple reasons. Custody of tokenized fund shares is a new revenue line. Distribution of tokenized funds through banking channels expands client offerings. And tokenized money market fund units can be used as collateral for derivatives — a use case with significant institutional demand, since MMF units are recognized as eligible collateral but historically too slow to transfer for margin purposes. Tokenization solves the speed problem.

For a deeper treatment of how fund tokenization works, the step-by-step process, and detailed real-world examples, see our comprehensive guide to tokenized funds and our Fund Tokenization report.

D. Digital Asset Custody

Every tokenization use case described above depends on one foundational capability: the ability to securely custody digital assets on behalf of clients. Without custody infrastructure, a bank can't offer tokenized products, can't hold tokenized fund shares for investors, and can't participate in tokenized settlement networks.

Digital asset custody is fundamentally different from traditional securities custody. It's not just about safekeeping — it's about managing the cryptographic keys that control assets on a blockchain, while also handling smart contract interactions, enforcing governance policies, supporting multiple blockchain networks, performing asset servicing (staking, corporate actions, distributions), and maintaining complete audit trails.

The governance dimension is especially critical for banks. A custody platform must support granular controls — multi-approval workflows, role-based access, segregation of duties — down to individual smart contract functions. A bank's regulatory compliance team needs to be able to define exactly who can authorize a token transfer, who can execute a mint or burn, and under what conditions, with every action logged and auditable.

This is where Taurus' core offering, Taurus-PROTECT, sits. Taurus-PROTECT is a banking-grade digital asset custody platform built with defense-in-depth security (HSM, MPC, and TSS cryptographic techniques), granular governance that extends to the smart contract function level, and support for hundreds of digital assets across 21+ native blockchain protocols. It can be deployed on-premise, as a managed service, or in a hybrid model — a critical requirement for large banks with strict data residency and operational control requirements.

Deutsche Bank selected Taurus-PROTECT as its digital asset custody infrastructure. State Street announced a strategic agreement with Taurus to deliver digital asset capabilities for its institutional clients — a partnership that won Digital Asset Partnership of the Year at the 2025 Global Custodian Leaders in Custody Awards. CACEIS, the asset servicing arm of Crédit Agricole and Santander, uses Taurus for custody and tokenization. ClearBank, a UK clearing bank, chose Taurus-PROTECT as its wallet infrastructure to support stablecoin services, integrating it with Circle Mint for MiCAR-compliant USDC and EURC. Pictet, the Swiss private bank and Taurus Series B investor, also deploys the platform.

Taurus also co-authored the CMTA Digital Asset Custody Standard — the first industry-wide custody standard for digital assets — alongside the Capital Markets and Technology Association. The standard defines the security, operational, and governance requirements that institutional custody solutions should meet.

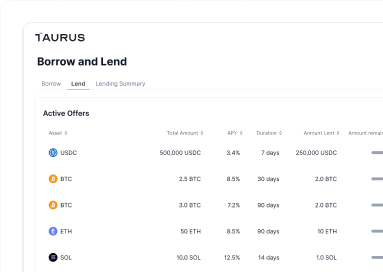

E. Interbank Settlement and Collateral Management

The highest-value layer of banking tokenization is what happens between institutions: settling financial transactions and managing collateral using tokenized assets and tokenized cash.

Traditional interbank settlement involves multiple intermediaries, days of delay, and significant capital locked in clearing processes. Tokenized settlement enables atomic delivery-versus-payment — both legs of a transaction settle simultaneously or not at all — eliminating counterparty risk and freeing trapped capital. It also operates 24/7, removing the constraints of market hours and cut-off times.

JPMorgan's Tokenized Collateral Network is already live, allowing institutional clients to post tokenized collateral for derivatives margins. Swift has conducted multi-chain interoperability pilots with DTCC and Euroclear. Hong Kong's Monetary Authority has launched a tokenization pilot with HSBC, Standard Chartered, Bank of China, BlackRock, and Franklin Templeton participating.

Taurus-NETWORK was built specifically for this use case — an interbank network for settlement and collateral management of digital assets. It connects banks, exchanges, and liquidity providers to settle financial transactions, post and manage collateral, and trade directly from cold storage. The network carries zero network-operator counterparty risk, meaning Taurus itself never takes custody of participant assets.

The Technology Infrastructure Banks Need

Participating in tokenization requires a technology stack that most banks didn't have five years ago. The core components are:

Digital asset custody — secure private key management meeting banking-grade standards, with multi-blockchain support, granular governance (multi-approval, role-based access, segregation of duties), and full audit trails. This is the foundation everything else depends on.

A tokenization engine — the ability to deploy smart contracts, configure token parameters, and manage the full lifecycle of tokenized assets: minting, burning, transferring, freezing, unfreezing, whitelisting, and corporate actions. Must support multiple smart contract standards (CMTAT, ERC3643, ERC1400) and multiple blockchains.

Trading and settlement infrastructure — regulated venues for secondary market trading of tokenized assets, and settlement rails that connect on-chain token movement with off-chain fiat payment. Automated delivery-versus-payment is the benchmark.

Compliance and governance — on-chain transfer restrictions enforced via whitelisting, AML scoring of blockchain addresses, and integration with the bank's existing regulatory compliance stack.

API connectivity — tokenization infrastructure must integrate with existing core banking systems (Temenos, Avaloq, and others), risk platforms, and regulatory reporting tools. Banks can't operate digital assets in a silo disconnected from their existing operations.

Deployment flexibility — banks have strict data residency, security, and operational requirements. The platform must support on-premise, cloud/managed service, or hybrid deployment models.

Taurus' platform covers this full stack through four integrated products: Taurus-PROTECT (custody), Taurus-CAPITAL (tokenization and lifecycle management), Taurus-PRIME (trading, including a FINMA-regulated organized trading facility), and Taurus-NETWORK (interbank settlement and collateral management). The platform is built on 100% proprietary technology, fully API-based, and already in production with over 40 regulated financial institutions.

Building a Bank Tokenization Strategy: Where to Start

Banks at different stages of readiness can enter tokenization at different points. While multiple tracks can be pursued in parallel, each layer builds on the capabilities established by the previous one.

1. Start with custody. This is the foundation and can generate revenue from day one — offering crypto custody services to existing institutional clients while building internal competency with the technology, key management, and governance workflows.

2. Add tokenized deposits or stablecoin capabilities. Banks with a custody foundation can introduce tokenized deposits for internal settlement (interbranch transfers, corporate treasury management) before offering them externally. This creates the "cash leg" needed for on-chain settlement of other tokenized assets.

3. Issue tokenized securities. With custody and tokenized cash in place, banks can begin issuing tokenized bonds, structured products, or equity for clients, with automated lifecycle management through smart contracts.

4. Offer tokenized fund services. This includes acting as custodian for tokenized fund shares, providing transfer agent services, or distributing tokenized funds through existing banking channels.

5. Connect to interbank settlement and collateral networks. The highest-value layer, where tokenized assets flow between institutions for settlement, repo, and collateral management. This requires all prior capabilities to be in place and delivers the largest operational efficiency gains.

Regulation

Switzerland was the first Tier 1 financial center to adopt a complete DLT-compatible legal framework. Article 973d of the Swiss Code of Obligations (2021) recognizes ledger-based securities. FINMA-regulated organized trading facilities like Taurus-PRIME allow tokenized securities to trade while issuers retain their private company status. Banks can obtain licenses for crypto securities register services.

The European Union has established a multi-layered framework: MiCAR for stablecoins and crypto-assets, the DLT Pilot Regime for tokenized securities trading, and MiFID for classifying tokenized fund units as financial instruments. 37 European banks are forming a consortium to launch a MiCA-regulated euro stablecoin by mid-2026.

The United States is evolving rapidly. The GENIUS Act has provided regulatory clarity for stablecoins. SEC-registered tokenized funds are in operation. A consortium of major banks — including Goldman Sachs, Bank of America, Citi, Deutsche Bank, and UBS — is exploring a shared stablecoin pegged to G7 currencies.

Asia-Pacific is active through Singapore's Project Guardian (institutional pilots with UBS, SBI, and Chainlink) and Hong Kong's tokenization pilot (HSBC, Standard Chartered, Bank of China, BlackRock, Franklin Templeton).

The common thread: regulators are converging toward fitting tokenized versions of existing financial instruments under existing securities and banking law, rather than creating entirely new regulatory categories.

Challenges and Implementation Considerations

Tokenization in banking is production-ready, but the ecosystem is still maturing.

Interoperability between blockchains remains limited. Assets issued on Ethereum can't natively interact with those on other blockchains. Cross-chain bridges exist but add complexity and risk.

Legacy integration is the practical challenge every bank faces. Core banking systems — often decades-old mainframes running COBOL — can't be replaced overnight. Tokenization infrastructure must integrate through APIs with existing systems for payments, risk, reporting, and compliance.

Liquidity fragmentation is a real concern. Tokenized assets spread across multiple blockchains and trading venues may fragment rather than consolidate liquidity, undermining one of the core benefits.

Deposit stability risk deserves attention. The World Economic Forum has flagged the "paradox of programmability" — the instant transferability that makes tokenized deposits useful could also make bank deposit bases more volatile during stress events, as depositors can move funds in seconds rather than days.

The on-chain fiat gap is the most fundamental constraint. The full potential of tokenized settlement depends on having tokenized cash — whether through deposit tokens, regulated stablecoins, or CBDCs — available at scale to close the settlement loop entirely on-chain. This is being actively addressed by the bank consortiums and central bank initiatives described above, but it isn't solved yet.

Conclusion

Tokenization is no longer an innovation lab initiative. It's a core banking infrastructure upgrade that the world's largest institutions are deploying in production — for deposits, securities, fund shares, custody, and interbank settlement.

The competitive dynamics are clear. Banks that build custody, tokenization, and settlement capabilities now will define the next generation of financial infrastructure and capture the client relationships that come with it. Banks that wait will find themselves depending on the infrastructure built by those that didn't.

Taurus provides the integrated platform — custody, tokenization, trading, and interbank settlement — that banks need to launch and scale their tokenization strategies. Our technology is already in production with over 40 regulated financial institutions, including State Street, Pictet, CACEIS, and ClearBank. Whether you're starting with custody or ready to connect to an interbank settlement network, we can help you move from strategy to production.

To explore how Taurus can support your institution's tokenization strategy, book a meeting or download our tokenization whitepapers.